News

-

Dynamic Programming Volume II: General States Now Available books

13 Mar 2026

Volume II of Dynamic Programming by Thomas J. Sargent and John Stachurski is now available for free download.

Volume II: General States extends the finite state framework of Volume I to general state spaces, covering:

Part I: General Theory

- Abstract Dynamic Programs (Parts 1-3)

- Transforms

Part II: Models and Applications

- Concave DP Problems

- Risk-Sensitive Dynamic Programming

- Applications

The book is available as a free PDF download from the Dynamic Programming website, alongside Volume I and its accompanying code and slides.

-

Julia Lectures Now Available on Google Colab lectures

23 Feb 2026

The Quantitative Economics with Julia lecture series now supports running notebooks on Google Colab.

Instructions for getting started are available in the Running on Google Colab section of the Getting Started lecture.

-

New Tool: MyST Markdown Plugin for Neovim tools

17 Feb 2026

QuantEcon has released myst-markdown-tree-sitter.nvim, a Neovim plugin that provides syntax highlighting and filetype detection for MyST (Markedly Structured Text) markdown files.

The plugin extends standard markdown highlighting with MyST-specific features, including:

- Code-cell directive highlighting with language-specific syntax highlighting for

{code-cell}directives - Math directive highlighting with LaTeX syntax highlighting for

{math}directives - Automatic filetype detection for MyST markdown files based on content patterns

- Tree-sitter integration for robust parsing

- Comprehensive testing with 170+ tests

The plugin supports a wide range of languages in code-cell directives, including Python, Julia, R, JavaScript, and more.

For installation instructions and documentation, visit the project website.

- Code-cell directive highlighting with language-specific syntax highlighting for

-

New Julia Lecture: Differentiable Filters and Enzyme Updates lectures

9 Feb 2026

A new lecture has been added to Quantitative Economics with Julia: Differentiable Filters.

This lecture covers implementing and differentiating the Kalman filter using both forward-mode and reverse-mode automatic differentiation. It documents specific coding patterns needed to get high performance while remaining compatible with Enzyme.

A key challenge addressed in the lecture is that small, static immutable matrices call for a completely functional coding style, while large matrices require everything to be done in-place. Getting the same code to work efficiently in both cases requires careful design. Much of this is driven by Enzyme’s requirement for non-allocating code — which, fortunately, is usually aligned with highest performance anyway.

This release also updates the lectures to support the official Enzyme.jl release for Julia 1.12.

These updates were developed by Jesse Perla.

-

New Lecture: Gorman Aggregation with Heterogeneous Households lectures

28 Dec 2025

We’re pleased to announce a new lecture on Advanced Quantitative Economics with Python: Gorman Aggregation with Heterogeneous Households.

About the Lecture

This lecture explores one of the fundamental questions in macroeconomic theory: under what conditions can an economy with diverse households be analyzed as if there were a single representative consumer?

Key topics covered include:

- Gorman aggregation conditions: When household demand can be aggregated regardless of income distribution

- Linear Engel curves: The role of quasi-homothetic preferences in enabling aggregation

- Practical implications: Understanding when representative agent models are appropriate approximations

Why This Matters

Representative agent models are ubiquitous in macroeconomics, but their validity depends on specific conditions that aren’t always met. This lecture provides the theoretical foundations for understanding:

- When aggregation is justified

- What heterogeneity matters for aggregate outcomes

- How to think about distributional effects in macro models

The lecture includes computational examples and exercises to reinforce the theoretical concepts.

Contributors

This lecture was developed by Humphrey Yang and Thomas Sargent.

-

New Julia Lecture: Differentiable Simulations with Enzyme lectures

17 Dec 2025

We’re pleased to announce a new lecture on Quantitative Economics with Julia: Differentiable Dynamics.

This lecture demonstrates how to use Enzyme.jl for automatic differentiation of dynamic economic simulations. The code is more advanced than typical lectures — Enzyme requires non-allocating, functional-style code — but this is necessary to unlock high-performance differentiation of simulation models.

For readers looking for a gentler introduction to Enzyme, see the Introduction to Enzyme section in the auto-differentiation lecture.

Other Updates in This Release

- Julia 1.12 support with updated packages across all lectures

- Reorganized interpolation and integration lectures for improved flow

- Refactored Finite Markov chains lecture with clearer exposition

- Updated software engineering and testing content

These updates were developed by Jesse Perla and Farhad Shahryarpoor.

-

Workshop: Modern Computational Economics at the IMF workshop

2 Dec 2025

QuantEcon instructors Chase Coleman and John Stachurski delivered a three-day workshop on Modern Computational Economics and Policy Applications at the IMF headquarters in Washington, D.C. from December 2-4, 2025.

Building on the 2024 workshop, this year’s course placed greater emphasis on AI and its implications for economic policy analysis. Topics included:

- AI pair programming for economists

- JAX for high-performance dynamic programming

- Data wrangling with Pandas and Polars

- Bayesian analysis and Gaussian processes

- Deep learning and reinforcement learning

Workshop materials are available on GitHub.

-

New IFP Lectures with Wealth Inequality Analysis lectures

2 Dec 2025

The Quantitative Economics with Python series has been expanded with significant new content on income fluctuation problems and wealth inequality.

New Lecture Content

- Transient Income Shocks: A new lecture separating transient shocks from the core IFP model, providing clearer theoretical exposition

- Wealth Inequality Analysis: New exercises analyzing how return volatility and labor income volatility affect wealth distribution

- Stochastic Returns: Improved simulation methods for studying wealth dynamics under uncertainty

Key Findings Highlighted

The new content demonstrates important economic insights:

- Varying return volatility (capital income risk) has a much larger impact on wealth inequality than labor income volatility

- The lectures include Gini coefficient calculations showing how different parameter choices affect wealth distribution

Technical Improvements

- Performance optimizations using

jax.lax.while_loopfor better JAX compatibility - Cleaner code structure with improved function signatures and better variable naming

- Enhanced visualizations of wealth dynamics and distribution

These updates reflect ongoing research collaboration and were developed with contributions from John Stachurski.

-

Reorganized Optimal Savings and Parallel Programming Lectures lectures

25 Nov 2025

We’ve completed a significant reorganization of lectures across two of our Python lecture sites to improve content flow and learning progression.

Optimal Savings Lectures (python.quantecon.org)

The Intermediate Quantitative Economics with Python series has undergone a major restructuring of the optimal savings content:

- Renamed and reorganized the income fluctuation problem (IFP) lectures for clearer progression

- Added dynamics plots and adjusted parameters for better visualization

- Improved code organization with consistent function signatures across lectures

- Enhanced JAX implementations with unified operator signatures between standard and JAX versions

Parallel Programming Lectures (python-programming.quantecon.org)

The Python Programming for Economics and Finance site now features reorganized parallel programming content:

- Restructured table of contents for better topic flow

- Improved content on NumPy vs Numba vs JAX comparisons

- Better explanations of parallel computing concepts

These updates were developed with contributions from John Stachurski, Humphrey Yang, and Matt McKay.

-

Workshop: Computational Methods for Macroeconomic Modeling at Bank of Portugal workshop

7 Oct 2025

QuantEcon instructor John Stachurski delivered a four-day workshop on Computational Methods for Macroeconomic Modeling at the Bank of Portugal from October 7-10, 2025.

The workshop explored recent advances in scientific computing driven by AI hardware and software, including parallelization, automatic differentiation, and just-in-time compilation. Topics covered included:

- Python fundamentals for scientific computing

- Markov chains and dynamic programming

- Introduction to JAX for high-performance computing

- Neural networks and deep learning applications

Workshop materials are available on GitHub.

-

Closure of discourse.quantecon.org announcement

17 Mar 2025

The QuantEcon organization is closing the discourse forum (running since 2016) hosted at discourse.quantecon.org.

We have recently observed a large increase in spam posts. As the forum was not seeing high usage rates we felt the maintenance cost was higher than the benefit it was bringing to the broader community.

We are still dedicated to encouraging community linkages and discussion and will be evaluating new platforms and opportunities. We are also looking at developing AI tutors for our lecture sites.

Thank you to everyone that participated in the forums.

-

Jupyter Book is a Jupyter sub-project news

19 Feb 2025

The QuantEcon organization is a founding member of the Executable Books project that built Jupyter Book and MyST Markdown

We are really excited to share that Jupyter Book has now been accepted as a Jupyter sub-project.

-

Closure of notes.quantecon.org announcement

11 Feb 2025

For the past 6 years we have hosted an online community at notes.quantecon.org.

This was designed to be a place for the economics community to upload interesting notebooks and encourage linkages and discussion.

There have been some excellent notebooks uploaded, and we thank all the authors that have contributed to this community.

Unfortunately the notes platform (as currently designed) requires a server which is relatively expensive to run and maintain.

In addition there is a software maintenance burden to keep the underlying software called Bookshelf up to date.

As a result we have decided to close notes.quantecon.org.

To enable all these excellent notebooks to be accessible we have migrate all the current notebooks to a new static page hosted on GitHub.

We welcome any PRs to contribute any additional notebooks.

QuantEcon will continue to think of new and innovative ways to build a sharing community for notebooks on computational economics.

There is some work underway with the Jupyter Book team for gallery support that may offer hosting notebooks as a collection of static webpages, which is much cheaper to host.

We thank you for your interest and participation in QuantEcon Notes.

The Bookshelf project is open-source and will remain available for anyone interested in it.

-

QuantEcon workshop at the Reserve Bank of Australia workshop

22 Nov 2024

QuantEcon ran a workshop at the Reserve Bank of Australia presenting recent advances in computational tools available in open source scientific computing environments.

These new tools include:

- automatic differentiation

- parallel computing, and

- just-in-time compilers and GPU computing

-

QuantEcon RA working with Google Search news

2 Nov 2024

Congratulations to Smit Lunagariya for your new role at Google search. Smit was a former QuantEcon research assistant and contributed extensively to the QuantEcon project. We hope you enjoy your new role in the machine learning team.

-

QuantEcon workshop at the University of Melbourne workshop

15 Aug 2024

QuantEcon ran a workshop at the University of Melbourne presenting recent advances in computational tools available in open source scientific computing environments.

These new tools include:

- automatic differentiation

- parallel computing, and

- just-in-time compilers

-

Africa summer course 2024 workshop

8 Aug 2024

QuantEcon has delivered our Africa summer course in July/August 2024 across three universities in West Africa. Our aim is to bring the foundational skills required for working with more advanced computational economic models to a global audience. It was exciting for the team to be able to work with these talented students in West Africa.

-

QuantEcon workshop at Central Bank of Chile workshop

15 May 2024

QuantEcon ran a workshop at the Central Bank of Chile on high performance computing using Python and how Python can be used in economic applications.

-

QuantEcon Workshops at Columbia University and International Monetary Fund (IMF) workshop

30 Oct 2023

QuantEcon delivered two workshops this month. One at Columbia University and the other at the International Monetary Fund (IMF).

-

QuantEcon Africa summer course workshop

31 Jul 2023

QuantEcon has just delivered our Africa summer course in July across three universities in West Africa. Our aim is to bring the foundational skills required for working with more advanced computational economic models to a global audience. It was exciting for the team to be able to work with these talented students in West Africa.

-

Welcome to Our New Research Assistants news

25 Jun 2023

We would like to give a warm welcome to Porntipa Poonpolsub and Sreehari P. Sreedhar, who have joined QuantEcon as research assistants. Dia is first year Master of Computing student at ANU. Sreehari a data analysit who currently enrolled in Bachelor of Applied Data Analytics at ANU. They are helping improving QE lectures.

-

Introductory Lecture Series Launched lectures

14 Jun 2023

QuantEcon has launched A First Course in Quantitative Economics with Python, a first lecture series that introduces quantitative economics using elementary mathematics and statistics plus computer code written in Python and that emphasize simulation and visualization through code as a way to convey ideas, rather than focusing on mathematical details. A big thank you to Shu Hu, Smit Lunagariya, Matthew McKay, Maanasee Sharma, Humphrey Yang, Chien Yeh and Hengcheng Zhang, along with other research assistants at QuantEcon, for their invaluable contributions in creating these lectures.

-

New Book on Economic Networks news

5 Jun 2023

The new book “Economic Networks, Theory and Computation” by John Stachurski and Tom Sargent, will be published at Cambridge University Press. An online version can be found here.

-

Quantitative Economics with Google JAX lectures

31 May 2023

QuantEcon has launched Quantitative Economics with Google JAX, a new lecture series that introduces JAX and its techniques to solve high-dimensional economic problems. Google JAX is an open-source Python library developed by Google Research that provides a range of tools for fast linear algebra operations, automatic differentiation, and efficient parallel computing. JAX builds upon the popular NumPy library, extending it with additional features such as automated GPU and TPU support, just-in-time compilation, and efficient optimization and estimation. The lectures cover applications such as asset pricing problems, inventory dynamics, and wealth distribution dynamics. A big thank you to Shu Hu, Smit Lunagariya, Matthew McKay, Humphrey Yang, Hengcheng Zhang, and Frank Wu, along with other research assistants at QuantEcon, for their invaluable contributions in creating these lectures.

-

New book on dynamic programming news

13 May 2023

The new book “ Dynamic Programming Volume 1” by Tom Sargent and John Stachurski is available here.

The book is about dynamic programming and its applications in economics, finance, and adjacent fields like operations research. It brings together recent innovations in the theory of dynamic programming and also provides related applications and computer code.

-

QuantEcon Workshops in Japan workshop

5 May 2023

-

Welcome to Our New Research Assistants news

1 Apr 2023

We would like to give a warm welcome to Frank Wu and Hengcheng Zhang, who have joined QuantEcon as research assistants. Frank is a master student of computing at ANU and has a bachelor in information technology at ANU. Hengcheng has just received his Bachelor of Science with majors in mathematics and computer science. They are assisting with new QE lectures.

-

RSE Computational Economics Workshop workshop

2 Feb 2023

On February 16 2023, QuantEcon hosted a workshop designed to introduce students and policy makers to modern scientific computing tools and their applications to economic problems. The workshop was led by Thomas J. Sargent and John Stachurski and held in the Research School of Economics at Australian National University. The workshop featured attendees from policy institutions such as the Reserve Bank of Australia and the Australian Treasury, highlighting the increasing importance of computational skills in economic policy and research. Material from the workshop can be found on GitHub.

-

Recently Added Lectures lectures

9 Jan 2023

We have been busy adding new material to our Python lectures site.

Using Newton’s Method to Solve Economic Models finds the equilibrium of a supply and demand model using convergence algorithms such as Newton’s method. The lecture demonstrates Newton’s method for one-dimensional and multi-dimensional settings, and implements the algorithm using JAX to solve a very high-dimensional problem.

Job Search VII: A McCall Worker Q-Learns extends earlier lectures on the McCall model to introduce Q-learning. This algorithm allows us to assume the worker has less knowledge about the wage generation process and reward function.

Finally, Non-Conjugate Priors provides a sequel to an earlier lecture that compared Bayesian and frequentist interpretations of probability. In our new lecture, we look at techniques used when the prior and posterior distribution over parameters do not share the same functional form (are not conjugate).

-

Introducing Our Research Assistant Smit Lunagariya news

1 Nov 2022

We would like to introduce Smit Lunagariya who has been working as a Research Assistant at QuantEcon since April 2022. Smit is a Masters student at the Indian Institute of Technology and is writing his thesis on Quantitative Economics under the guidance of Thomas J. Sargent and John Stachurski. He has contributed to several projects at QuantEcon, including the QuantEcon.py library, QuantEcon lectures, and worked as a Teaching Assistant for QuantEcon’s workshops in India. Smit has been an outstanding Research Assistant at QuantEcon and his contributions have been highly valued.

-

Updates to NumPy and Advancing Programming in Python Lectures lectures

30 Sep 2022

We have updated our NumPy lecture to include a discussion of how broadcasting in NumPy makes code faster and less memory-intensive. We have also added a section on variable names to the Advanced Programming in Python lecture. This section looks at local, builtin, and global namespaces in Python, how to view namespaces and name resolution rules. Many thanks to our research assistant Humphrey Yang for his improvements to the lectures.

-

Dynamic Structural Econometrics Conference 2022 workshop

25 Aug 2022

QuantEcon co-founder John Stachurski will provide a sequence of lectures on computational dynamic programming at the next Econometric Society summer school in Dynamic Structural Econometrics, which will be held at the Australian National University, Canberra over 13-19 December 2022. The conference and summer school theme is Methodology and applications of dynamic structural models with strategic interactions. More information can be found on this page.

-

Welcome to Our New Research Assistant news

7 Aug 2022

We would like to give a warm welcome to Maanasee Sharma, who has joined QuantEcon as a research assistant. Maanasee is a Masters student at the Delhi School of Economics and has a Bachelors in Mathematics from the Lady Shri Ram College for Women. She will be assisting with new QuantEcon lectures and textbook material, as well as acting as a Teaching Assistant for QuantEcon’s online intensive course this August. We look forward to having Maanasee part of our team!

-

QuantEcon Summer Course at the African School of Economics workshop

4 Aug 2022

QuantEcon held a two-week summer course in Quantitative Economics at the African School of Economics (ASE) from July 11 - 22, 2022. The course was attended by talented young economists from the ASE and the Institute of Statistics and Applied Economics (ENSEA). Course content included introductory Python, data science with Pandas, linear algebra, optimization, high performance computing and macroeconomic applications. More information about the workshop and materials can be found on this page.

-

Upcoming QuantEcon Workshops in Canberra and Paris workshop

7 Jul 2022

QuantEcon will hold a workshop in computational economics at Australian National University, Canberra on July 22, 2022. The workshop is open to students from the College of Business and Economics and is targeted towards graduate students at the start of masters or PhD programs, or advanced undergraduates who want to boost their computing skills. Further details and workshop materials can be found in the GitHub repository.

Later this year, QuantEcon is holding a three-day workshop in computational economics at the Center for Research in Economics and Statistics in Paris beginning on September 12. The workshop invites PhD students and interested researchers to attend, with accommodation expenses partially covered for PhD students traveling to Paris. Further details can be found in the workshop’s GitHub respository.

-

Updates to Exercises in Python Lectures lectures

14 Jun 2022

Using new functionality from sphinx-exercise, QuantEcon Python and Python programming lectures now include styled exercises and hides exercise solutions by default. sphinx-exercise v0.4 introduces gated directives, allowing code in exercises and solutions to be nested within the lecture while still being executable. The sphinx-exercise documentation has been updated with more information about the gated syntax.

-

Protecting Privacy in Randomized Surveys lectures

12 May 2022

Two new lectures discuss how to protect respondents’ privacy while accounting for selection biases in randomized surveys. Randomized Response Surveys provides an introduction to using probability to design a survey such that the designer is unaware of individuals’ responses, particularly when they may belong to a stigmatized group. Expected Utilities of Random Responses considers how to optimally design a survey with privacy protections using an expected utility approach.

-

Comparing Bayesian and Frequent Approaches lectures

9 Mar 2022

A new lecture titled “Two Meanings of Probability” compares Bayesian and Frequentist approaches to estimating parameters of a distribution. Using Python to simulate random draws from a binomial distribution, estimating the parameters using the Frequentist approach is shown to converge to the true parameters by the Law of Large Numbers. Similarly, as a Bayesian observes more random draws from the binomial distribution, they become more confident about the true value of the parameters. The lecture provides several exercises for the reader to test their knowledge of these two approaches to probability.

-

QuantEcon Lectures Now Support Julia 1.7 news

23 Feb 2022

Quantitative Economics with Julia has been updated to support the latest version of Julia (v1.7). This update follows significant changes to the Julia side of the lectures in September 2021. Many thanks to Jesse Perla, his team, and support from the Center for Innovative Data in Economic Research (CIDER) at the Vancouver School of Economics at the University of British Columbia.

-

New Lecture on First-Price and Second-Price Auctions lectures

16 Feb 2022

A new Python lecture on first- and second-price sealed-bid auctions of a single good has been added. The lecture sets up and solves for an agent’s optimal bid given their valuation, and proves with a numerical example that the Revenue Equivalence Theorem holds — that is, the expected revenue of both types of auctions are equal. In the case where closed form solutions cannot be found, the lecture provides a method to simulate an agent’s optimal bidding strategy. A subsequent lecture on multiple good auctions relaxes the single-good assumption and considers a simultaneous, multiple-good, ascending-price auction.

-

Julia Lectures Updated lectures

8 Sep 2021

The Quantitative Economics with Julia lectures have been given a significant update.

Beyond infrastructure updates, the lecture notes now more strongly software engineering concepts, such source code control and collaboration and test-driven development and continuous integration. We see these as essential steps towards reproducible research, and the skills are transferable across programming languages.

Some of the key changes:

- Source code and Jupyter Notebooks fully support Julia 1.6, and will soon support Julia 1.7 after its release.

- A significant revamp of the setup process now focuses on an early introduction of Git, GitHub and VS Code.

- The lecture on Julia Tools and Editors lecture has moved to VS Code and provides additional workflows in support of the Git and GitHub.

- The GitHub, Version Control, and Collaboration lecture shows workflows for collaboration within VS Code and GitHub.

- All content in the Packages, Testing, and Continuous Integration lecture now uses GitHub Actions as the continuous integration framework, and shows the VS Code workflows required for reproducible research and collaboration.

- The lectures are now using Jupyter Book. Among other things, the move to the markdown format makes open-source contributions and bug fixes even easier.

We are grateful for support from the Center for Innovative Data in Economic Research (CIDER) at the Vancouver School of Economics at the University of British Columbia.

-

NYU Computational Social Science Certificate Program workshop

24 Jul 2021

Tom Sargent, Chase Coleman, and Spencer Lyon have put together The NYU Computational Social Science: Certificate Program. It uses many quantecon resources. The program aims to prepare students for either a graduate program in the social sciences or for a career as a data analyst or computational social scientist.

-

Data Science Student Project Showcase news

14 May 2020

QuantEcon is showcasing the 2020 student projects taught with the QuantEcon Data Science lecture series.

The students covered

- Python Fundamentals

- Scientific Computing and Economics

- Introduction to Pandas and Data Wrangling

- Data Science Case Studies and Tools

Many of the students had limited to no exposure to programming prior to the course. These projects are a testimony to their hard work.

You can see the collection here

-

Python Lecture Series Split lectures

7 Apr 2020

QuantEcon has divided its main Python lecture series into three parts to help guide our readers through the series. This split was carried out in response to requests from many readers to make the lectures more accessible, and to provide more guidance on the order in which lectures should be read.

The first series is called Python Programming for Quantitative Economics. These lectures teach Python from basics and foundations to advanced, high-performance features, including just-in-time compilation and parallelization.

The second series is called Introductory Quantitative Economics with Python. This part covers solving and simulating fundamental economic models using Python and a range of modern algorithms. It is suited to advanced undergraduates and first year graduate students.

The third series is Advanced Quantitative Economics with Python. This series builds on the introductory lectures and is suited to a graduate students and practitioners.

-

Julia Lectures Updated to 1.3 news

9 Mar 2020

The QuantEcon Julia lectures have been updated to use Julia 1.3. Additionally, the new Julia version has been installed on associated cloud servers, such as

quantecon.syzygy.ca.The release comes with performance improvements and bug fixes that we are happy to add to the lectures. -

QuantEcon (ANU) PreDoc Position for 2020 news

4 Nov 2019

The QuantEcon Early Career Researcher in Computational Economics will support development of the QuantEcon project and the Principal Investigator. The project is a benchmark for high quality open source code for the economic sciences and supports quantitative economic analysis in all branches of the discipline. The QuantEcon project is coordinated by researchers at New York University and Australian National University. The position is located at The Australian National University, College of Business and Economics, Research School of Economics. Candidates should have a long-term interest in pursuing economics related research and are looking to undertake a PhD.

Role

Under the broad direction of Principal Investigator the Early Career Researcher will:

- Assist in the development of lectures at http://lectures.quantecon.org/

- Assist in development of QuantEcon code libraries

- Provide day to day assistance to QuantEcon team members

- Outreach to community including possible travel in support of QuantEcon workshops

- Participation and assistance of lectures, forums and cloud related infrastructure

- Comply with all ANU policies and procedures, and in particular those relating to work health and safety and equal opportunity

Selection Criteria

- A degree in computer science, economics or closely related field

- Ability to use Unix / Linux / OS X

- Knowledge of Python

- Awareness of Open Source development tools.

- Some knowledge of web development (CSS,HTML) LaTeX and/or Julia programs

- Ability to engage in collaborative project activities, and working as part of a team

- Excellent communication skills.

- Must have Australian work rights.

- A demonstrated understanding of equal opportunity principles and policies and a commitment to their application in a university context

This position is a 1 Year fixed term contract.

Application Process:

Applications can be submitted to ANU Recruit. This page will be updated with a submission link once applications are open. If you are interested in this position please email your CV to QuantEcon as an expression of interest.

Applications Close: 12th January 2020

Please contact John Stachurski for more information.

-

Global PDF restored on for the Python lectures news

30 Jun 2019

For the first time in many months, we have a PDF available in book form for the entire collection of Python lectures. The build procedure uses Sphinx to convert our RST files to Jupyter notebooks, executes them, and then runs pandoc over the results to generate LaTeX. Custom Python code then builds the result into a single book. A big thanks to Anju Joon for taking on this huge task and successfully completing it.

-

Demand curve estimation with pyBLP lectures

17 Jun 2019

One of the most important quantitative problems in economics is demand curve estimation in differentiated product markets. The best known modern algorithm is the so-called BLP method, due to Steven Berry, James Levinsohn and Ariel Pakes. In a significant step forward for computational modeling, Chris Conlon and Jeff Gortmaker have developed a sophisticated Python implementation called pyBLP. A corresponding set of notebooks can be found at QE notes.

-

Announcing our new intern: Welcome Anju Joon news

14 May 2019

We would like to give a warm welcome to Anju Joon, who has joined QuantEcon as a summer intern for 10 weeks from May of 2019. Anju is an undergraduate student studying economics and mathematics at IIT Kharagpur, India and an active part of the Student Welfare Group. We are delighted to have her on the team, and to help her further build her strong programming and analytical skills.

-

QuantEcon pre-doc Natasha Watkins starting at UCLA news

3 May 2019

Congratulations to QuantEcon pre-doctoral fellow Natasha Watkins, who has been accepted to the PhD program at UCLA in 2019! Natasha has been a key part of the QuantEcon team since March 2017, following a year at the Reserve Bank of Australia. During her time, she has contributed lectures including Linear Regression in Python and Maximum Likelihood Estimation, and assisted running workshops in Australia, New Zealand, Europe, China and the US. We are delighted to see her continuing her studies in economics and look forward to future contributions to the QuantEcon project!

-

Run Quantecon Lectures With Google Colab

11 Apr 2019

layout: post title: “Run QuantEcon Lectures with Google Colab!” author: Natasha Watkins excerpt: You can now open a lecture as a Jupyter notebook in Google Colab, allowing code to be run and edited live in the cloud. tag: [news]—

You can now open a lecture as a Jupyter notebook in Google Colab, allowing code to be run and edited live in the cloud. Simply click the ‘Run Notebook’ button in the top left-hand corner to launch the notebook in Colab (you will need to be signed in with a Google account).

Colab is a free service provided by Google that runs in your browser – requiring no local installation. The majority of libraries used in our lectures come pre-installed in Colab – the remaining libraries are installed with a pip command at the start of the lecture.

-

Workshop for the Department of Industry, Innovation and Science workshop

5 Apr 2019

On April 10th 2019, QuantEcon will run a one day workshop at Australian National University on Python for computational economics and econometrics. The workshop is aimed at beginners to Python, although some prior coding experience in other programming languages is preferable.

For more information, see this page.

-

Summer School in Dynamic Structural Econometrics 2019 workshop

1 Mar 2019

Application deadline: April 15, 2019

Submissions: http://dseschool.orgLecturers include: Günter J. Hitsch, Fedor Iskhakov, Michael Keane, Sanjog Misra, Robert A Miller, John Rust and Bertel Schjerning

Applications are now open for the Econometric Society’s Summer School in Dynamic Structural Econometrics (DSE). The summer school will be held at Booth School of Business and the Becker Friedman Institute for Economics at the University of Chicago from July 8 to July 14, 2019.

The primary focus of DSE summer schools is to provide students with tools and “hands on” computational instruction to carry out research in applied microeconometrics with strong emphasis on closely integrating economic and econometric theory in empirical work. We will discuss state-of-the-art methods for solving, simulating and estimating dynamic programming models and use a variety of empirical applications to illustrate how these tools and methods are used in practice.

The 2019 Econometric Society DSE summer school consists of 5 days of lectures held in conjunction with the 3rd Conference on Structural Dynamic Models (July 10- 11, 2019). Besides the core components, including single agent models, equilibrium models, and dynamic games, the course will also feature applications that follow the special theme of this year’s conference, “Industrial organization, marketing and business analytics.”

The DSE summer school and conference takes place in conjunction with the six week Open Source Economics Laboratory Boot Camp at the University of Chicago.

Interested students are invited to submit their applications via the summer school website http://dseschool.org before April 15, 2019. Students interested in also attending the full 6 week boot camp should submit applications to the OSM website https://www.oselab.org before March 15, 2019.

All applicants must be a member of the Econometric Society at the time of application. To join the Society, go to the home page of the Econometric Society, http://www.econometricsociety.org.

-

Apply to OSE Boot Camp 2019 workshop

20 Feb 2019

The Open Source Economics Laboratory (OSE Lab) at the University of Chicago is excited to announce that we are now accepting applications for the 2019 OSE Lab six-week summer boot camp in computational economics, July 1 to August 9, 2019, at the University of Chicago. This is our third year supporting the boot camp, and the OSE Lab has funding for 25 student positions. Students can get more information and submit an application from the following page. The application deadline is Mar. 15, 2019.

https://www.oselab.org/bootcamp/2019

Each admitted OSE Lab student will receive a $4,000 stipend, lodging, and airfare to and from Chicago. Admissions are competitive, and we welcome applications from advanced undergraduate students, masters students, and PhD students. All students will also get to participate in the Econometric Society’s Dynamic Structural Economics Workshop and Conference, July 8-14, at the University of Chicago.

Prerequisites for participating in the camp are multivariable calculus, linear algebra, real analysis, calculus based microeconomic theory (constrained optimization with Lagrange multipliers), and some computer programming experience (e.g., Python, R, C++, Fortran, Java) or software languages (e.g, MATLAB, STATA). Most of the programming in the Boot Camp will be in Python.

Leadership and Instructors

This year’s camp is organized by Richard Evans (University of Chicago) and Simon Scheidegger (HEC Lausanne). Other OSE Lab instructors at this summer’s boot camp include Lars Hansen (University of Chicago), Anthony Smith, Jr. (Yale University), John Rust (Georgetown University), and Felix Kubler (University of Zurich).

Curriculum

The economics portion of this year’s curriculum will include continuous and discrete choice dynamic programming, structural estimation, numerical integration and derivatives, dynamic games, and machine learning.

The numerical methods curriculum will include numerical derivatives and numerical integrals, matrix decomposition (SVD, eigenvalues-eigenvectors, QR-LU), unconstrained and constrained numerical optimization (root finders and minimization), dimension reduction.

The computational curriculum will include object oriented programming, unit testing, Git and GitHub collaboration workflows, visualization techniques, and two weeks of training in high performance computing and parallel programming using the University of Chicago’s Midway supercomputing cluster.

Past years’ curricula are available in the 2018 Boot Camp repository and in the 2017 Boot Camp repository.

Contact and Questions

We hope that many excellent students apply. Additional details on the boot camp and program are available on the OSE Lab website (www.oselab.org). Feel free to send any questions to Richard Evans (rwevans@uchicago.edu) or Simon Scheidegger (simon.scheidegger@unil.ch).

-

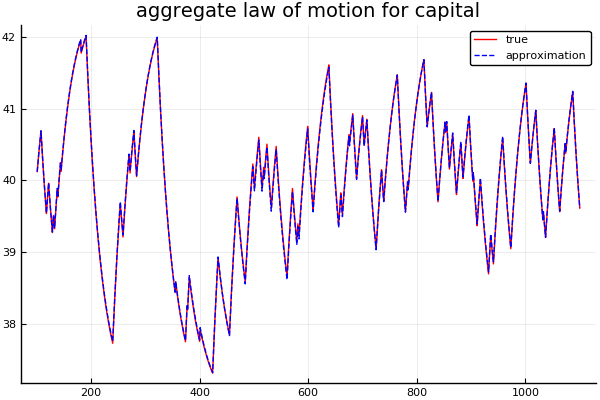

Krusell-Smith Model with Julia lectures

24 Jan 2019

This notebook shows how to solve the Krusell-Smith model using the Euler equation method in Julia, in addition to replicating an example from Maliar, Maliar, and Valli. Solving the model yields the aggregate law of motion for capital.

-

Major Update to Build System news

11 Jan 2019

Over the past year, the QuantEcon team has been working on a major update to the QuantEcon lecture build system. For a reader, the changes are not obvious – lectures are still styled to appear as Jupyter notebooks, and feature integrated testing implemented at the end of 2018.

Under the hood, the lecture build system has changed substantially, and it is now easier to maintain and update lectures. Output cells are automatically generated from code, meaning that updates to packages used in the lectures will be reflected on the site. We intend to improve on this foundation through advances in Continuous Integration testing, coverage statistics for error tracking, and migrating execution control to the sphinxcontrib-jupyter package.

We have continued to work on Jupinx, our tool to generate Jupyter noteboook from RST files. Notebooks with full lecture content are now available for download on each lecture page.

QuantEcon is thankful to Matt McKay for his hard work on this update.

-

Partnership with University of British Columbia news

11 Dec 2018

QuantEcon is partnering with the Centre for Innovative Data in Economics (CIDE) at the University of British Columbia (UBC) to collaborate on open-source software and online textbooks in computational economics. As a first step, Jesse Perla and his team at UBC have worked to revise and update the Julia version of our lectures. CIDE and QuantEcon’s collaborative efforts will also help the Vancouver School of Economics offer a new undergraduate course on data science and machine learning in economics in January 2019.

For more information, please see the press release from UBC.

-

Speeding up the Python Lectures lectures

5 Dec 2018

QuantEcon has been working to speed up the Python lectures with the help of just-in-time compilation from Numba. Just-in-time (jit) compilation allows code to be compiled on the fly - a flexible combination of ahead-of-time compilation and interpretation (standard Python is interpreted).

By jitting the lectures, we’ve seen speed improvements of about 1 to 2 orders of magnitude. A discussion of the benefits of Numba with Python is in No, Python is Not Too Slow for Computational Economics.

The majority of jitted lectures use fixed point iteration to find the model’s solution, some examples include The Stochastic Optimal Growth Model, The Lucas Asset Model and Search With Learning.

Thanks to Natasha Watkins for work on this improvement.

-

Julia 1.0 Lectures Released lectures

4 Dec 2018

As part of the move to Julia 1.0, QuantEcon lectures in Julia have been significantly revised and are now co-authored with Jesse Perla at the University of British Columbia. QuantEcon welcomes Jesse and his team to the project, and is excited about the changes on the Julia side.

Improvements include:

- The addition of many new lectures, for example on version control with GitHub and generic programming in Julia.

- An update to the Julia cheatsheet.

- The creation and use of new QuantEcon packages, such as Expectations.jl and InstantiateFromURL.jl.

- The integration (and development) of outside packages such as Parameters.jl, NLsolve.jl, and Optim.jl, which we used to write clearer and faster code.

- An overhaul of the infrastructure used to build and deliver the lectures.

We are thankful to Arnav Sood, and Jose Calderon for their work on the content side, and Matt McKay for the build infrastructure. Also thanks to Kaan Yolsever, Adam Jozefiak, Xiaojun Guan and Pooya Ravari for their research assistance on this project.

-

QuantEcon.py 0.4.2 Released news

27 Nov 2018

The latest release of QuantEcon.py implements the Abreu and Sannikov algorithm for solving games efficiently, as demonstrated in this notebook. We have also added a just-in-time compiled Nelder-Mead algorithm for multivariate optimization. Thanks to Zejin Shi and Quentin Batista, among others, for their work on this release.

-

QuantEcon Merchandise Store news

22 Oct 2018

In collaboration with NumFOCUS, we have launched a merchandise store featuring QuantEcon-branded goodies such as stickers, tshirts, hats, and more. Purchases from our merchandise store will help support and promote the QuantEcon project.

-

QuantEcon Notes Officially Launched news

19 Oct 2018

QuantEcon is excited to launch QuantEcon Notes, a site for sharing and viewing Jupyter notebooks related to computational economics. QuantEcon Notes allows users to submit their own notebooks to share with a collaborative community. Notebooks that reproduce results from published papers using open code and data are welcome, as are original observations and comments. Read more about the launch here.

-

Inaugural NumFOCUS Awards Dinner news

3 Oct 2018

Congratulations to Jesse Perla, who was recognized at the inaugural NumFOCUS Awards Dinner for his contributions to QuantEcon. Jesse has recently coordinated and contributed to QuantEcon’s efforts to support Julia 1.0. Jesse’s knowledge of our online lectures, having used QuantEcon materials to teach a class at University of British Columbia, has been invaluable to improving their usefulness for users. As part of this work, Jesse has also involved new research assistants to help build the infrastructure and test the lectures.

-

QuantEcon.jl v.15.0 Released news

10 Sep 2018

Following the much anticipated release of Julia 1.0, QuantEcon.jl has been updated with full compatibility for 1.0. After installing Julia 1.0, you can update QuantEcon.jl by opening Julia’s new package manager (Pkg) and typing

add QuantEcon

We are thankful to José Bayoán Santiago Calderón for his hard work on this release.

-

QuantEcon.py v0.4 Released news

21 Aug 2018

The latest update of QuantEcon.py (v0.4) adds Numba jitted root finding methods - part of our effort to provide fast, just-in-time compiled code across our code base. Additionally, a Hamilton filter function and several updates to the game theory module were merged. Full release notes can be found here.

Thank you to all the developers who contributed to this update.

-

Robust Markov Perfect Equilibrium Lecture Added lectures

8 Aug 2018

A new lecture extending Markov Perfect Equilibrium and Robustness lectures has been added to the Python side here. The lecture was co-authored by Doncheng Zou. The lecture produces plots that compare previous results to the model with robust decision rules; the new model features a higher price path and lower output path. Additionally, the lecture considers equilibrium effects when firms have heterogenous beliefs about output and price.

-

Fiscal Risk and Government Debt Lecture Added lectures

24 Jul 2018

A new Python lecture studying government debt over time has been added to our dynamic programming squared section. The lecture builds on previous optimal taxation lectures (here and here) and extends them to an economy with three Markov states. In the long-run, this economy exhibits behaviour close to that described in the two-state case. The new lecture can be found here.

-

Casual Lead Web Developer Position news

30 May 2018

QuantEcon is looking for a part-time lead web developer to continue active development of the QuantEcon Notes (http://notes.quantecon.org) project. Notes is a user generated website focused on sharing Jupyter notebooks and fostering discussion related to economics research.

More information about the position can be found here.

Applications close 10th June 2018.

-

Pathways for QuantEcon Lectures lectures

4 May 2018

We have added tabs to the table of contents (also on the julia side) on the lectures site that allow students to select material suited to either undergraduate or graduate level. Additionally, we have refined our lectures listing, with new categories for dynamic programming and time series models.

Tabs allow you to select a course suited to your skill level.

-

QuantEcon Honours Workshop recap workshop

23 Mar 2018

Over 30 Honours students from around Australia attended the QuantEcon Honours workshop at Australian National University on March 10th, 2018. The workshop covered modern methods in computational and dynamic modeling, and included a lecture from Tom Sargent during his visit to Australia. Students learned the basics of Python for scientific computing, as well as dynamic programming and economic applications to quantum computing.

Details of the workshop and materials can be found here.

Tom Sargent presenting at the 2018 QuantEcon Honours Workshop.

-

Updates to the lectures site lectures

19 Mar 2018

Due to our growing number of lectures, we have revised the table of contents (python / julia) into more specific topics such as dynamic programming and time series.

Additionally, we have split our original McCall Search Model lecture into two parts. The first lecture (julia version) uses a basic McCall model to introduce learners to dynamic programming. Part II (julia version) extends this model to include job separation.

These changes are a part of our effort to accommodate less advanced users of our website — more changes are to come.

-

QuantEcon.py v0.3.8 Released news

15 Mar 2018

The latest release of QuantEcon.py (v0.3.8) includes a new function for drawing random variables (PR #397) and a number of updates to the game theory module, including the ability to generate a graph of a random tournament (PR #378). A full list of updates can be found here.

To update QuantEcon.py via pip, use

pip install --upgrade quanteconThanks to oyamad, QBatista, mcsalgado, and okuchap for their contributions in this release.

-

Applications for OSM Boot Camp 2018 workshop

16 Feb 2018

Applications are open for the 2018 Open Source Macroeconomics Lab Boot Camp. The boot camp will be held at the University of Chicago from June 18 to August 3.

The program is open to talented and motivated advanced undergraduate students and graduate students, with 25 fully funded student slots available for summer 2018. Funding includes travel to and from the University of Chicago, housing at the University, and a stipend of $4,200 for the seven weeks.

Successful applicants will have taken courses or demonstrate proficiency in core microeconomic theory (constrained optimization with Lagrangian), linear algebra, multivariable calculus, real analysis, and writing code in some programming language.

More details can be found here.

-

Honours Workshop with Thomas J. Sargent workshop

1 Feb 2018

On March 10th 2018, QuantEcon will run a one day workshop on modern methods in computational and dynamic modeling, aimed at incoming honours students in economics across Australia. The workshop, to be held in Canberra, will include a lecture from and discussion with 2011 Nobel Laureate in Economic Sciences Thomas J. Sargent. Topics will include an introduction to scientific computing with Python, basic principles of software engineering and an introduction to macroeconomic and financial modeling using computational techniques. Funding for travel and accommodation will be offered to selected interstate students. Further details can be found here.

To apply, please send your CV and a discussion (up to one page) of why you believe computational skills are important for economic modeling to contact@quantecon.org. Applications close Thursday, February 15th. (Note: ANU economics Honours students need not apply and should register their attendence with this form).

-

QuantEcon is Hiring in 2018 news

31 Jan 2018

Term Length: Fixed Term, 12 Months

- Contribute to an exciting new open-source project building computing tools for research in economics

- Work within a global team based at ANU and NYU

- Opportunity to develop skills before heading to a PhD

The QuantEcon Early Career Researcher in Computational Economics will be responsible for providing support in the development of the QuantEcon project (https://quantecon.org). The QuantEcon project consists of lectures and code libraries designed to teach quantitative skills and solve quantitative economic problems. The code libraries contain routines for optimization, control, simulation and estimation that are motivated by economic problems and written in Python and Julia.

The position is funded by QuantEcon but located at The Australian National University, College of Business and Economics, Research School of Economics. Candidates should have a long-term interest in pursuing economics related research and are looking to undertake a PhD.

A position description is available here.

Applications close February 25. Please apply here: http://jobs.anu.edu.au/cw/en/job/519358/quantecon-research-assistant-in-computational-economics

For more information please contact John Stachurski at john.stachurski@anu.edu.au

-

Welcoming New Steering Committee Members news

27 Jan 2018

QuantEcon welcomes Richard Evans and Daisuke Oyama as new steering committee members. Richard is the Director of the Open Source Macroeconomics Laboratory and holds positions at the University of Chicago and the Becker Friedman institute. Daisuke is a Professor at the University of Tokyo and has made many valuable contributions to the QuantEcon library. We are delighted to have them on our team.

-

Download Lectures as Jupyter Notebooks news

12 Jan 2018

Every QuantEcon lecture now features a button like the one shown above that enables you to download code from the lecture in a Jupyter notebook. The notebooks are generated using Jupinx, a tool we released late last year to convert reStructuredText files (the format we write our lectures in) to Jupyter notebooks. Notebooks are tested daily and therefore should run sequentially without errors. You can check the execution status of notebooks here.

-

Thomas Sargent Keynote Presentation at PyData NYC workshop

4 Jan 2018

Thomas Sargent’s keynote presentation from PyData NYC 2017 is now available on Youtube. The talk, titled ‘Economic Models’, is aimed at people without an economics background and gives an overview of economists’ approach to modeling. The talk discusses some of the problems economists face when using models for policy analysis, and the importance of having an underlying theory to make inferences from data.

-

QuantEcon Blog and Jupinx Launch news

11 Dec 2017

We’ve just launched the QuantEcon blog to share more information about the work we do at QuantEcon and provide greater insight into the tools we use. Our first post, Introducing Jupinx, details the new Sphinx extension we’ve developed to allow users to easily convert text files to Jupyter notebooks. If you’d like to install Jupinx or contribute to the package, you can find information on the GitHub repository. Thanks to Matthew McKay, Akira Matsushita, and Nick Sifniotis for their hard work on Jupinx.

-

Code Testing on Lecture Site news

31 Oct 2017

QuantEcon has implemented automatic code testing on the lecture website! The code testing tool, developed by Matthew McKay, Akira Matsushita and Nick Sifniotis, runs every code snippet embedded in the site nightly on our build server. Errors trigger an alert to the QuantEcon team, allowing us to fix them as they occur. We’ll document and open source this tool in the coming weeks.

-

Conclusion of PhD Workshop Series workshop

15 Sep 2017

QuantEcon finished its PhD workshop series at UC San Diego today. Overall, we had close to 400 registrations for the workshops at 8 different universities in the United States. Workshop attendees were introduced to Jupyter notebooks, open source programming in Python and Julia, and computational methods for economics. We hope the workshops will encourage new PhD students to use open source tools in their studies. Material from the workshops can be found here.

-

QuantEcon.py Updated news

29 Aug 2017

QuantEcon.py has been updated to v0.3.6.2. This update brings new features in the game theory module and docstrings with better math rendering, among other minor improvements.

-

ANU Lab Space Refurnishment news

25 Aug 2017

As part of the QuantEcon-RSE Joint Initiative at Australian National University, the QuantEcon lab space in the Copland building is being updated and refurnished. Pictured below are new signs outside Room 1130 in the Copland building. The room houses several QuantEcon research assistants and visitors, and is welcome to be used by faculty members in computational economics.

-

Linear Regression in Python lectures

24 Jul 2017

A new lecture covering linear regression in Python has been added. The lecture uses the Python packages statsmodels and linearmodels to replicate results from Acemoglu, Johnson and Robinson’s paper, ’The colonial origins of comparative development’. We have also rearranged our lectures index on the Python side, and expect to add more content to the Data and Empirics section in the near future.

-

QuantEcon RSE Joint Initiative news

23 Jun 2017

QuantEcon is pleased to be a part of a joint initiative in computational economics with the Research School of Economics at Australian National University. The QuantEcon RSE joint initiative is a collaboration with researchers at RSE, and will support research and teaching in computational economics. QuantEcon is grateful for the continued support offered by RSE. For more information, please see here.

-

2017 PhD Workshops in Computational Economics workshop

23 Jun 2017

QuantEcon will be running free 1-day workshops in computational economics at a number of US universities in September 2017. The workshops are targeted at economics PhD students and faculty, and will provide an overview of modern open source tools and techniques for computational modeling. For for more information about where we are attending and registration, please see here.

-

Need for Speed in Julia lectures

29 May 2017

We have published a new lecture titled The Need for Speed on the Julia side of the website. The lecture covers how to write high performance code by using Julia’s just in time compilation, type inference, and multiple dispatch features. This lecture follows on from an earlier Julia lecture, Types, Methods and Dispatch.

-

Workshop on Bayesian modeling with Jim Savage workshop

23 May 2017

QuantEcon is sponsoring Jim Savage to present a workshop on modern statistical workflow and Bayesian modeling in Stan. The workshop will be held at the Australian National University on 19 June. For more information, please see here.

-

Introducing our 2017 summer intern news

23 May 2017

QuantEcon welcomes our newest member, Trevor Lyon (@tlyon3 on Github), who is currently visiting the Australian National University in Canberra. Trevor is an undergraduate computer science student at Brigham Young University. He will be spending the summer working on various QuantEcon projects, including our new notebook publishing site.

-

Pandas for panel data lectures

28 Apr 2017

An additional lecture on Pandas has been added that covers more advanced functions such as merging, grouping, and using multiindices. Pandas is a powerful Python package that contains useful tools for working with large and complicated datasets. The lecture specifically focuses on techniques useful for working with panel data, with applications to datasets from the OECD and Eurostat.

-

Statistics comparison cheatsheet lectures

24 Apr 2017

If you’re considering making the switch over to Python from STATA (or even R), we have a new cheatsheet to help you do so! The cheatsheet compares commonly used functions for data handling and manipulation across STATA, Base R, and the Pandas package for Python.

-

Sequential Analysis in Julia lectures

10 Apr 2017

A Julia version of A Problem that Stumped Milton Friedman is now available. The lecture covers sequential analysis - a technique developed by Abraham Wald to solve decision making problems.

-

Endogenous Grid Method in Python and Julia lectures

7 Apr 2017

We have added a new lecture (in both Python and Julia) on the endogenous grid method for policy iteration. The EGM algorithm, invented by Chris Carroll, results in significant speed improvements over Coleman policy function iteration.

-

New Julia Lectures and Style Update lectures

28 Mar 2017

You can now find three new lectures on the Julia side of QuantEcon lectures covering Globalization and Cycles, Coleman Policy Iteration, and the Lake Model. Additionally, the lectures’ style has been refreshed to make reading code input and output simpler.

-

RBA and RBNZ QuantEcon Workshops workshop

21 Mar 2017

Following the lead of the Federal Reserve Bank of New York (FRBNY), an increasing number of central banks have expressed interest in converting their DSGE modeling implementations to Julia. To help meet this demand, QuantEcon ran workshops at the Reserve Bank of Australia and the Reserve Bank of New Zealand on the 10th and 13th of March 2017. They were presented by John Stachurski (QuantEcon and ANU), Pablo Winant (Bank of England), Erica Moszkowski (FRBNY) and Pearl Li (FRBNY). The workshops introduced central bank employees to the Julia programming language and its uses in macroeconomic modeling. Slides from the workshop can be found in the QuantEcon GitHub repository.

-

OSM Boot Camp at the University of Chicago workshop

18 Jan 2017

The Open Source Macroeconomics Laboratory (OSM Lab) at the Becker Friedman Institute is soliciting applications for a seven week computational macroeconomics boot camp for advanced undergraduate students and some graduate students, to be held at the University of Chicago from June 19 to August 4 of 2017. Funding is available to successful applicants and the QuantEcon lectures will be part of the curriculum. Applications must be submitted by February 17. For further details see http://bfi.uchicago.edu/osm.

-

QuantEcon is hiring in 2017 news

12 Jan 2017

Position descriptions are now available for a PostDoc and a PreDoc. These positions are based at The Australian National University (ANU) in Canberra, Australia. Please send any expressions of interest to contact@quantecon.org

-

Migrating from Google Groups to Discourse Forum news

21 Nov 2016

QuantEcon is migrating from the Google Groups based forum to a new discussion forum built on Discourse. The new forum is located at http://discourse.quantecon.org/ and is also linked through the QuantEcon org and lecture websites. Please feel free to join the conversation, make suggestions for improvements, or tell us what project you’d like to see the QuantEcon team work on next.

-

Keynote lecture at JuliaCon 2016 news

29 Oct 2016

A few months ago one of us (the one who’s better at fly fishing) gave a lecture on macroeconomics and computational methods at JuliaCon. The video can be found here. The talk provides a quick overview of the state of modern macroeconomics. It is aimed at a general audience with a background in computation, but will likely be of interest to some economists as well. Discussion centers on formation of beliefs and expectations, modeling of markets and technologies, and associated computational challenges.

-

Julia version of Aiyagari lecture lectures

9 Aug 2016

A Julia version of the Aiyagari lecture has been added to the site. The code was written by NYU PhD student Victoria Gregory. We are also grateful to contributions from Maximilian Huber and Spencer Lyon.

-

QuantEcon will be hiring developers soon news

8 Jul 2016

As mentioned in an earlier news item, QuantEcon has received a large new grant from the Alfred P. Sloan Foundation. Among other things, the grant will allow us to hire a postdoctoral fellow, a pre-doctoral fellow, part time web developers and many new RAs. We will be looking for highly talented programmers with experience using Python, Julia and other open source tools. Formal announcements will go out shortly. In the meantime, please feel free to send your CV and informal expressions of interest to contact@quantecon.org.

-

New grant awarded by the Sloan Foundation! news

1 Jul 2016

We are delighted to announce that QuantEcon has received a very generous additional round of funding from the Alfred P. Sloan Foundation. The grant will support many new and existing activities over the coming years. Along with further development of the lecture site and code libraries, we have major plans for revamping the notebook gallery in order to make it more interactive, for building new code libraries, and for supporting a variety of open source scientific projects based around Python and Julia.

-

QuantEcon has joined NumFOCUS news

1 Jun 2016

Along with several collaborators, we have created an organization called QuantEcon to coordinate developement and documentation of open source software for economists. This lecture site now falls under the QuantEcon umbrella, as a QuantEcon sponsored project. QuantEcon has been accepted as a member of NumFOCUS, a nonprofit that supports open source scientific software development. Other members of NumFOCUS include IPython, Julia, Matplotlib, NumPy, pandas and Jupyter. QuantEcon is run for the benefit of the economics community, and contributions of code, documentation, ideas or developer time are most welcome. The QuantEcon website provides information for anyone who would like to get involved.

-

Workshop at Econometric Society meetings workshop

12 Feb 2016

On June 16 we’ll be running a workshop based around quant-econ.net at the North American summer meeting of the Econometric Society. The workshop will provide a quick start introduction to programming in Python and Julia for economists. The target audience is economists with some experience with programming in Matlab, Stata or similar, who are curious about Python and Julia, and how they might be useful for research in quantitative economics. The workshop page contains further details.

-

Notebook gallery added to the QuantEcon site news

22 Dec 2015

We’ve added a notebook gallery to the QuantEcon organization site in order to collect interesting Jupyter notebooks related to quantitative economics. Please feel free to submit your notebook for possible inclusion. Instructions are available on the notebook page.

-

NY Fed's DSGE model ported to Julia news

5 Dec 2015

I’ve seen the future of central bank forecasting and it’s written in Julia (to paraphrase Jon Landau). That’s right, with a small amount of help from the team at QuantEcon, the FRBNY has converted its main DSGE model from Matlab to Julia. Moreover, the code has been posted on GitHub, a public repository hosting service. This means that anyone can fork their code, mess around with it and suggest changes, using the full power of the open source development ecosystem. This seems like a big win for transparency and open science, while at the same time shifting the FRBNY code base to a cutting edge language and delivering significant speed gains.

-

Python site updated to Python 3.5 news

2 Dec 2015

The entire Python side of the website has now been updated to Python 3.5, along with all code examples. Our build environment is based on the latest Python 3.5 version of Anaconda. Apart from all the other goodies, this environment includes the

@operator for matrix multiplication, which comes with NumPy 1.10 and above. -

New lecture on discrete DP lectures

15 Sep 2015

A new lecture on discrete dynamic programming has been added to the the Python side of quant-econ.net. It demonstrates how to exploit some very high quality code for solving infinite horizon discrete dynamic programming problems written by Daisuke Oyama. We plan to develop a Julia version over the next few months. Please get in touch if you are interested in helping out on porting this code to Julia.

-

New lecture on uncertainty traps lectures

13 Sep 2015

A new lecture on uncertainty traps has been added to the the Python side of quant-econ.net. (Hopefully we’ll get a Julia version up before too long.) The lecture studies a simplified version of a very interesting model due to Pablo Fajgelbaum, Edouard Schaal, and Mathieu Taschereau-Dumouchel. The model shows how self-reinforcing uncertainty can have large impacts on economic activity.

-

New lecture on default risk lectures

2 Sep 2015

We have added a new lecture on the Python side on default risk and income fluctuations. The lecture computes versions of Cristina Arellano’spopular and important model of sovereign default. A Julia version of the lecture should be out in the next few days.

-

New on-line documentation news

5 Aug 2015

Largely thanks to the efforts of our RAs Chase Coleman and Spencer Lyon, we now have a shiny new on-line documentation page for QuantEcon.

-

QuantEcon website up news

10 Dec 2014

Our lectures draw heavily on code from two parallel code libraries, QuantEcon.py and QuantEcon.jl. These libraries have been unified under the QuantEcon project, and a website for the project is now up and running. The code libraries are separate entities from the lectures and are constructed in the usual open source way. All manner of contributions are welcome, from documentation improvements and minor bug fixes to new algorithms and models. More details can be found here. Thanks to Matt McKay and Andrij Stachurski for most of the leg work in getting the new website on line.

-

Julia now supported! news

3 Oct 2014

After a fair bit of work we’re finally ready to set loose on the world a Julia version of our lectures, as well as a nice new front end for the website. Most credit goes to our talented RAs Chase Coleman, Spencer Lyon and Matt McKay. Credit for the new website design and implementation goes to Andrij Stachurski.

-

Alfred P. Sloan Foundation grant awarded news

16 Jun 2014

We are delighted to announce that the Alfred P. Sloan Foundation has awarded quant-econ a very generous and helpful grant to support its development. The grant will allow us to spend a large amount of time working together over the coming years, with the objective of building up the code libraries and adding many new applications in all fields of economics and econometrics. It will also fund travel, workshops and conference presentations, and allow us to employ a postdoctoral fellow and a number of research assistants.

We feel very fortunate to be partnering with the outstanding team at the Sloan Foundation, and look forward to seeing quant-econ develop into a important resource for all economists.

-

Code library reorganizing news

10 Jun 2014

The past few weeks have been spent reorganizing the code library, combining the most useful programs into a package called QuantEcon. In practice this means that you can now

import quantecon as qe, in just the same way that youimport numpy as np. The package can be found on [pypi](https://pypi.python.org/pypi/quantecon/. Details and installation instructions can be found here.Like the great majority of Python libraries, QuantEcon is open source and we welcome contributions of high quality code for solving important economic models.